")

")

- Home

- About Us

- Our Products

- KGF Equity Backed Guarantees

- Treasury Backed Guarantees

- ACTIVE SUPPORT PACKAGES(2023)

- EXPORT SUPPORT PACKAGE

- INVESTMENT SUPPORT PACKAGE

- SUPPORT PACKAGE FOR OPERATING EXPENSES

- INVESTMENT-PROJECT FINANCE SUPPORT PACKAGE

- MANUFACTURING INDUSTRY SUPPORT PACKAGE

- OPERATING EXPENSES SUPPORT PACKAGE FOR 6 FEBRUARY EARTHQUKES

- INVESTMENT SUPPORT PACKAGE FOR 6 FEBRUARY EARTHQUAKES

- SUPPORT PACKAGE FOR SEVERANCE PAYMENT OF RETIREMENT AGE VICTIMS

- REGIONAL SME SUPPORT

- SUPPORT PACKAGE FOR ACTIVITIES GENERATING FX-BASED INCOME

- SUPPORT PACKAGE FOR WOMEN ENTREPRENEURS

- ENTREPRENEUR SUPPORT PACKAGE

- SUPPORT PACKAGE FOR GREEN TRANSFORMATION AND ENERGY EFFICIENCY

- TECHNOLOGY SUPPORT PACKAGE

- SUPPORT PACKAGE FOR DIGITAL TRANSFORMATION

- EDUCATIONAL SUPPORT PACKAGE

- ACTIVE SUPPORT PACKAGES(2022)

- Other >

- Export Support Package

- Cold Air Units And Frigorific Vehicles Support Package

- Investment Support Package

- Additional Employment Support Package

- Manufacturing Based Import Substitution Support Package

- (KOBI DEGER LOANS)

- Treasury Fund (32,5 Billion TL)

- Treasury Fund (52,5 Billion TL)

- Treasury Fund (200 Billion TL)

- EKONOMI DEGER LOANS

- (KOBI DEGER LOANS II)

- TOBB NEFES LOAN 2020 SUPPORT

- ACTIVE SUPPORT PACKAGES(2023)

- Our Supports

- Information Center

- Press

- Contact Us

WHAT IS KGF?

KGF acts as a guarantor for SMEs and non-SME enterprises that cannot get a loan due to insufficient collateral. KGF supports SMEs and non-SME enterprises in access to financing.

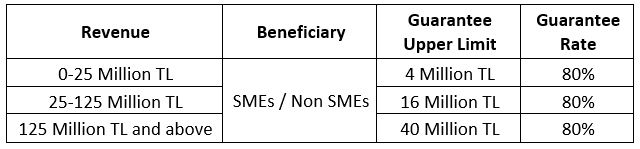

EKONOMI DEGER LOANS

Product Description

KGF will provide guarantee to the loans to be used by SMEs that cannot access financing for lack of guarantee in types and nature sought by banks. Guarantee limits per SMEs vary depending on their 2018 annual revenue

Source of the Guarantee

Treasury Fund

Relevant Organization/Financial Institutions

13 Banks holding shares in KGF A.S. (Halkbank, Ziraat Bankası, Vakıfbank, Garanti BBVA, TEB, Akbank, QNB Finansbank, Denizbank, Şekerbank, Eximbank, Yapı ve Kredi Bankası, İş Bankası, Alternatif Bank)

Maturity

The grace period is maximum 6 months, the total maturity is max 48 months with equal installments.

Guarantee Limit and Guarantee Rate

Fee and Commission

At the time of request for a letter of guarantee, the bank charges the beneficiary a one-off guarantee commission at a rate of 2% (two percent) of the guarantee amount for each disbursement of guarantee. 1.5% of this amount gets collected by KGF while the remaining amount is labelled as Treasury cut.

After charging 1% (one percent) of the guarantee amount from beneficiaries in restructured loan transactions, the Bank transfers the same to the account of KGF. 3% of this amount gets collected by KGF while the remaining amount is labelled as Treasury cut.

Application Requirements

General Criteria

- Beneficiaries are required to be one of the individual proprietorships or legal entity businesses established in accordance with the laws of the Republic of Turkey, operating at home or in Free Zones in Turkey.

- There should be no decision of bankruptcy, liquidation, suspension of bankruptcy or composition for bankruptcy from the companies in which at least 25% of the shares are owned by the beneficiary or by the beneficiary and/or his/her partners jointly or individually.

- The beneficiary should not have any overdue debt to the tax Office under the Article 22/A of the Law on Collection Procedure of Public Receivables dated 21/07/1953, no 6183, nor to the Social Security Institution under the Article 90, paragraph six of the Social Security and Universal Health Insurance Law dated 31/05/2006, no 5510, as documented by a letter dated within the last 90 days at the time of the loan disbursement, (where the debt has been restructured, the restructuring must not have been broken), where there is a debt within this scope, it must be restructured and the restructuring must not be broken, failing which such debts must be paid as a priority through the loan provided with KGF collateral provided that the debt in question does not exceed 20% of the loan,

- According to the most recent Credit Limit, Credit Risk and Receivables to be Liquidated Report issued by the Banks Association of Turkey Risk Center by the date of application to the Bank, the Beneficiary should not be classified in the category of non-performing loans under the "Regulation on the Principles and Procedures Governing the Classification of Loans and Other Receivables by Banks and Corresponding Reserves to be Provided for Them", nor should be classified under receivables monitored in the account "Past-Due Loans and Receivables Qualified as Loss" under the provisions of the Regulation on Accounting Practices and Financial Statements of Financial Leasing, Factoring and Financing Companies published in the Official Gazette dated 24/12/2013 and numbered 28861,

- The loans to be allocated to beneficiaries under this Protocol is subject to the requirement that there should be no unpaid commission debt from previous periods.

BUSINESS CONTINUITY SUPPORT

Product Description

The Ministry of Treasury and Finance has allocated a guarantee limit to Kredi Garanti Fonu. SME and non-SME enterprises will be made available until 31.12.2020.

In order to working capital needs of these enterprises and maintain their employment level by providing KGF guaranteed loan support to the enterprises which was affected by the COVID-19 epidemic, without any discrimination on sector.

Source of the Guarantee

Treasury Fund

Relevant Organization/Financial Institutions

5 Banks holding shares in KGF; T.C Ziraat Bankası, Türkiye Vakıflar Bankası, Türkiye Halk Bankası, Ziraat Katılım Bankası, Vakıf Katılım Bankası

Maturity

The grace period is maximum 6 months, the total maturity is max 36 months with equal installments.

Guarantee Limit and Guarantee Rate

Fee and Commission

- KGF collects one-time and in advance 0.75% of the amount of the guarantee for each guarantee from the beneficiaries in exchange of guarantees through banks. In the case of loan structuring, commission is collected from the beneficiaries in advance at 0.5% over the guarantee balance. In loan structuring processes made until 31.12.2020, no commission is charged in case the Treasury guarantee risk does not increase and the maturity of the guarantee risk does not extend more than 6 months.

- The Bank may charge an annual commission from the beneficiaries only for a maximum of 0.75% of the loan amount for each loan

- The Bank cannot demand any fees, fees and commissions under any name other than those mentioned in this heading, and the expenses they will pay for the transactions they will make to third parties (appraisal, insurance, etc.) from the loans they will provide within the scope of the Treasury-supported KGF guarantee.

Application Requirements

General Criteria

- Beneficiaries are required to be one of the individual proprietorships or legal entity businesses established in accordance with the laws of the Republic of Turkey, operating at home or in Free Zones in Turkey.

- There should be no decision of bankruptcy, liquidation, suspension of bankruptcy or composition for bankruptcy from the companies in which at least 25% of the shares are owned by the beneficiary or by the beneficiary and/or his/her partners jointly or individually.

- According to the most recent Credit Limit, Credit Risk and Receivables to be Liquidated Report issued by the Banks Association of Turkey by the date of application to the Bank, the Beneficiary should not be classified in the category of non-performing loans under the "Regulation on the Principles and Procedures Governing the Classification of Loans and Other Receivables by Banks and Corresponding Reserves to be Provided for Them", nor should be classified under receivables monitored in the account "Past-Due Loans and Receivables Qualified as Loss" under the provisions of the Regulation on Accounting Practices and Financial Statements of Financial Leasing, Factoring and Financing Companies published in the Official Gazette dated 24/12/2013 and numbered 28861,

- The loans to be allocated to beneficiaries under this Protocol is subject to the requirement that there should be no unpaid commission debt from previous periods.

OPERATING EXPENSES SUPPORT

Product Description

The Ministry of Treasury and Finance has allocated a guarantee limit to Kredi Garanti Fonu. SME and non-SME enterprises will be made available until 31.12.2020.

In order to working capital needs of these enterprises and maintain their employment level by providing KGF guaranteed loan support to the enterprises affected by the COVID-19 epidemic, without any discrimination on sector.

Source of the Guarantee

Treasury Fund

Relevant Organization/Financial Institutions

14 Banks holding shares in KGF; Türkiye İş Bankası, Türkiye Garanti Bankası, Yapı ve Kredi Bankası, Akbank, Denizbank, QNB Finansbank, Kuveyt Türk Katılım Bankası, Türk Ekonomi Bankası, Albaraka Türk Katılım Bankası, Türkiye Finans Katılım Bankası, Türkiye Emlak Katılım Bankası, ING Bank, Şekerbank

Maturity

Maturity is maximum 12 months, with a grace period is maximum 3 months.

Guarantee Limit and Guarantee Rate

Special Conditions

Expenses will be documented by contract or invoice.

Fee and Commission

- KGF collects one-time and in advance 0.5% of the amount of the guarantee for each guarantee for the use of the guarantee in exchange of guarantees. In the case of a configuration, a commission is collected from the beneficiaries in advance at 0.5% over the guarantee balance. In the configurations made until 31.12.2020, no commission is charged in case the Treasury guarantee risk does not increase and the maturity of the guarantee risk does not extend more than 6 months.

- In loans to be disbursed under the Treasury-funded KGF guarantee, the Bank cannot charge any additional fee other than the expenses to be paid for procedures to be fulfilled by third parties (appraisal, insurance etc.)

Application Requirements

General Criteria

- Beneficiaries are required to be one of the individual proprietorships or legal entity businesses established in accordance with the laws of the Republic of Turkey, operating at home or in Free Zones in Turkey.

- There should be no decision of bankruptcy, liquidation, suspension of bankruptcy or composition for bankruptcy from the companies in which at least 25% of the shares are owned by the beneficiary or by the beneficiary and/or his/her partners jointly or individually.

- According to the most recent Credit Limit, Credit Risk and Receivables to be Liquidated Report issued by the Banks Association of Turkey Risk Centre by the date of application to the Bank, the Beneficiary should not be classified in the category of non-performing loans except for loans classified in the third and fourth group under the "Regulation on the Principles and Procedures Governing the Classification of Loans and Other Receivables by Banks and Corresponding Reserves to be Provided for Them", nor should be classified under receivables monitored in the account "Past-Due Loans and Receivables Qualified as Loss" under the provisions of the Regulation on Accounting Practices and Financial Statements of Financial Leasing, Factoring and Financing Companies published in the Official Gazette dated 24/12/2013 and numbered 28861,

- The loans to be allocated to beneficiaries under this Protocol is subject to the requirement that there should be no unpaid commission debt from previous periods.