")

")

Product Description

This package is aimed at financing private educational institutions, as described in Article 2(1)(c) of Law No. 5580 on Private Educational Institutions, that face difficulties in meeting personnel expenses.

Resource for Guarantee

Treasury Fund

Related Financial Institutions / Corporations

Emlak Katılım Bankası, Halkbank, İş Bankası, Vakıfbank, Vakıf Katılım Bankası, Yapı Kredi Bankası, Ziraat Bankası, Ziraat Katılım

Product Maturity

Maximum 24 months maturity -Maximum 8 months grace period

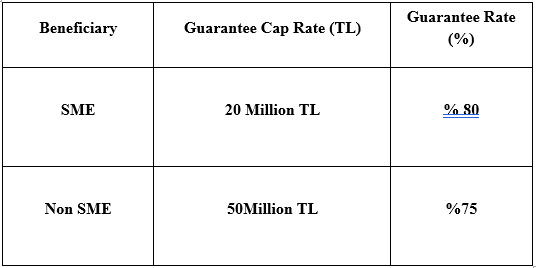

Guarantee Cap Rate and Guarantee Rates

Loan Products Available

- Business Credit Cards

- New Credit Card allocation

- Working capital loans that are to be disbursed to create a positive balance after making payments (including the following months) to a new Credit Card or existing Credit Cards that have no risk balance (Installment Loan, Spot Loan, Usury, etc.).

- Connected to a Debit/Bank Card;

- Overdraft Account (even if the beneficiary already has an account, a new overdraft account specific to this program must be opened)

- Installment Loan, Spot Loan, Usury, etc

- Working Capital Loan / Usury (*)

- Installment Loan

- Spot Loan

- Revolving Loan

- Cashless Overdraft Account products

- Other approaches suitable for Participation Banking

(*)Participation Banks may disburse loans through appropriate methods for participation banking, regardless of Debit/Business Card

Fee and Commission Rates

- The KGF shall collect, in return for each guarantee it gives, a one-time commission corresponding to 0.5% of the respective guarantee amount from the beneficiaries through the lenders. In the event of debt restructuring, a commission amounting to 0.5% of the balance amount of the guarantee shall be collected in advance from the beneficiaries through creditors.

- In retun for each loan disbursed, creditors may collect a commission amounting to a maximum of 1% of the loan amount from the beneficiaries.

Special Conditions

- Beneficiaries are required to commit to not reducing the number of employees for a period of two years from the date of loan disbursement.

- Credit cards will be restricted for cash advances.

- The sum of the gross salaries will be calculated by multiplying the amount stated in the last withholding tax return prior to the loan application date by 12. In addition, beneficiaries should prepare, and submit to the respective Creditor, monthly projections for the amount of the loan. Creditors will release the limit each month for the respective month’s gross salary payments (net salary plus related tax and SSI premiums). Beneficiaries must submit the necessary information and documents to the creditor regarding the payment of the previous month’s salary so that the creditor can release the limit.

- A maximum of 10% of the maximum 25% additional loan that can be allocated to the beneficiary can be given in cash to be used for operational expenditures

- Installment expenditures made by credit card cannot exceed the maximum 12-month disbursement period